Nasdaq futures nudged up 0.5% on Tuesday, extending Monday’s rebound as investors cautiously weighed the prospect of tariff relief against a backdrop of patchy economic data. Tesla, meanwhile, kept its foot on the accelerator, continuing its recent run after a sharp surge to start the week.

Tariff Talk Lifts Nasdaq Futures to Two-Week High

The tech-heavy futures settled at 20,517, their highest close in over a fortnight, building on Monday’s gains that reignited risk appetite across the broader market. Much of the optimism stemmed from reports that President Donald Trump is considering a phased approach to tariffs, with exemptions for select countries potentially set to be announced next week. That faint glimmer of flexibility was enough to stir some bullish sentiment, even if traders remain wary.

“Investors are cautiously optimistic, but the uncertainty around tariffs and ongoing geopolitical tensions is keeping a lid on risk appetite,” said Daniela Hathorn, senior market analyst at Capital.com.

In short: there’s hope, but it’s hedged. And with trade headlines still doing most of the heavy lifting, the market mood remains fragile at best.

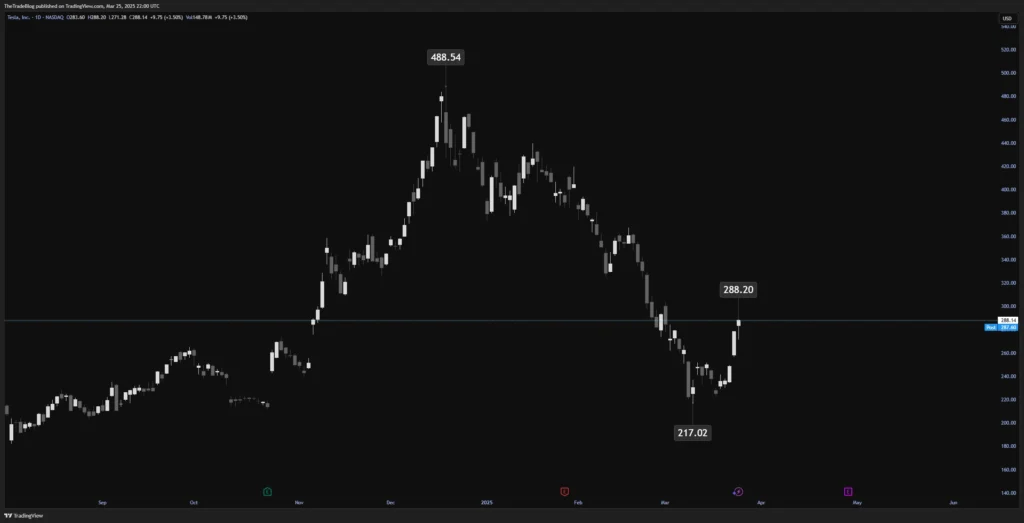

Tesla Stock Rally Continues, but Growth Concerns Persist

Tesla shares climbed for a second straight session, closing at $288.14 on Tuesday after Monday’s 11.9% jump. The latest push appears to be riding the wave of CEO Elon Musk’s internal message urging employees to “hold on to their Tesla stock”. That sentiment has done more for morale than most investor notes in recent memory.

But for all the bullish energy, context still matters. The stock remains deep in the red year-to-date. Persistent concerns around softening demand and intensifying competition, particularly in China and Europe, continue to cast a long shadow over the rally.

Semiconductor Stocks Pull Back as Nvidia Faces China Pressure

The broader tech space was a mixed bag on Tuesday. Semiconductor stocks, which had surged at the start of the week on reports of potential tariff exemptions for critical chip components, gave back some ground as the initial optimism faded. Nvidia bore the brunt of the pullback, coming under pressure once more amid persistent concerns over U.S. export restrictions to China. It’s a geopolitical thorn that continues to complicate the sector’s outlook.

U.S. Economic Data Mixed as Consumer Confidence Falls

Investors had plenty to chew on Tuesday as a new round of U.S. economic data landed. The headline figure was the Conference Board’s consumer confidence index, which dropped sharply to 92.9 in March from 100.1 in February. This marked the lowest reading in four years and added weight to growing concerns that consumer spending, a key pillar of the U.S. economy, may be losing steam.

Last week’s Federal Reserve decision remained front of mind, with policymakers keeping rates steady at 4.25% to 4.50%. While reiterating their data-dependent approach, officials also acknowledged a growing sense of economic uncertainty. Treasury yields barely flinched. The 10-year benchmark held firm at 4.25 as of 19 March.

Recent data points have offered little clarity. The services sector showed strength, with the S&P Global Services PMI rising to 54.3 in March from 51.0 in February. Manufacturing, on the other hand, dipped into contraction at 49.8, an unwelcome surprise that complicates the broader narrative.

Forecast Cuts Add Pressure Ahead of Final Q4 GDP Release

All eyes are on Thursday’s final reading of U.S. fourth-quarter GDP for 2024, alongside a trio of closely watched figures: corporate profits, initial jobless claims, and the goods trade balance. While late-stage GDP revisions rarely deliver surprises, any hint of softness could stir fresh doubts about the resilience of the economy heading into mid-year.

Those doubts are already beginning to take shape in official forecasts. The OECD expects U.S. growth to moderate to 2.2% in 2025, easing further to 1.6% in 2026. Weaker global trade, tighter financial conditions, and retreating fiscal support are among the risks it flags. Morgan Stanley takes a more downbeat view, trimming its 2025 estimate to 1.5% from an earlier 1.9%. The bank cites a cooling labour market and flagging consumer demand as reasons for its revised call.

Whether this points to a soft landing or something less graceful is still up for debate. Either way, investors may not have the luxury of sitting on the fence much longer.